Hayfin today announces that it has appointed Michaela Campbell as a Managing Director in its Private Credit team.

Michaela will be responsible for overseeing the team’s portfolio monitoring and risk profile across new and existing investments. She will be based in Hayfin’s headquarters in London and work closely with Portfolio Manager and Co-Head of Direct Lending, Mark Bickerstaffe and Portfolio Manager and Co-Head of Direct Lending, Marc Chowrimootoo.

Michaela’s appointment comes as Hayfin continues to deploy significant capital through its flagship private credit strategy, having last year exceeded its €6 billion target fundraise for Hayfin Direct Lending Fund IV. Recent investments across Hayfin’s private credit strategies include loans supporting IK Partners’ acquisition of French fire safety company Eurofeu Group and Näder Holdings’ repurchase of a minority stake in leading global orthotics company Ottobock.

Prior to joining Hayfin, Michaela spent five years at BlackRock in the Risk and Quantitative Analytics team and most recently served as co-head of global investment risk for Private Credit and Private Equity. Before joining BlackRock, she worked at GE Capital for more than a decade, where she held several roles in London and Abu Dhabi with a focus on underwriting, portfolio management and restructuring of leveraged loans. She earned a BSc degree in statistics and actuarial science from the University of the Witwatersrand in Johannesburg and is a CFA Charter holder.

Mark Bickerstaffe said: “We are delighted to welcome Michaela to Hayfin as a new Managing Director in the private credit team. She brings with her a wealth of directly transferable skills and insight from her previous roles. Michaela joins Hayfin at an exciting time as we look to capitalise on the recent increase of institutional asset allocation towards private credit in Europe and build on our recent private financing success across the continent. Establishing a specialised portfolio monitoring team is an important step for us as we continue to grow the capacity and ambition of our Private Credit strategy.”

Michaela Campbell said: “Hayfin has experienced remarkable growth in recent years and has consistently proven that it can deploy capital at scale and at speed, whilst maintaining a conservative risk profile. Its unparalleled network and connections across the European market are equally impressive. I look forward to working alongside my new colleagues and industry partners across Hayfin’s Private Credit strategy.”

Hayfin’s core private credit strategies comprise Direct Lending, through which Hayfin invests in performing loans to primarily European middle-market companies; Tactical Solutions in which the firm has a flexible mandate to pursue opportunistic investments with credit-like risk profiles at enhanced returns; and Special Opportunities, where it invests flexibly in a range of unique opportunities across industries, markets and sub-strategies in situations where financing may be scarce.

Disclaimer: Past affiliations are not a reflection of current capabilities and past performance is not an indication of future results.

Within the European private equity secondaries market, single-asset GP-led transactions are anticipated to double, if not triple, in volume in the next three to five years. Hayfin’s Mirja Lehmler-Brown sits down with Private Equity International to discuss the attractive dynamics within the current market, as well as its expected evolution over the coming years.

Read the full commentary below.

Hayfin today announces that it has acted as the provider of senior-secured debt financing to support IK Partners’ acquisition of French fire safety company Eurofeu Group (“Eurofeu”) from CAPZA.

Founded in 1972, Eurofeu installs and maintains fire protection equipment, as well as fire protection systems, for business-to-business (B2B) clients predominantly. Eurofeu’s integrated manufacturing capabilities enable the company to provide a highly differentiated offering from its competitors. It benefits from strong product sale revenues as well as generating additional income from the maintenance of existing fire protection equipment and the supply of associated spare parts.

Eurofeu employs 1.850 workers across 42 agencies and two manufacturing sites, serving approximately 160,000 B2B clients across France.

Alban Senlis, Head of Hayfin Private Credit in France, commented: “We are delighted to have partnered with the Eurofeu management team and prominent private equity sponsor IK Partners to underwrite this debt financing, providing the flexibility, certainty and speed of execution to enable this significant acquisition. We look forward to working closely with IK Partners and Eurofeu throughout the next chapter of the company’s growth journey.”

The debt financing brings the firm’s total investment activity in France through its Direct Lending strategy to c. €3 billion deployed across more than 20 transactions in the past 5 years.

Summary

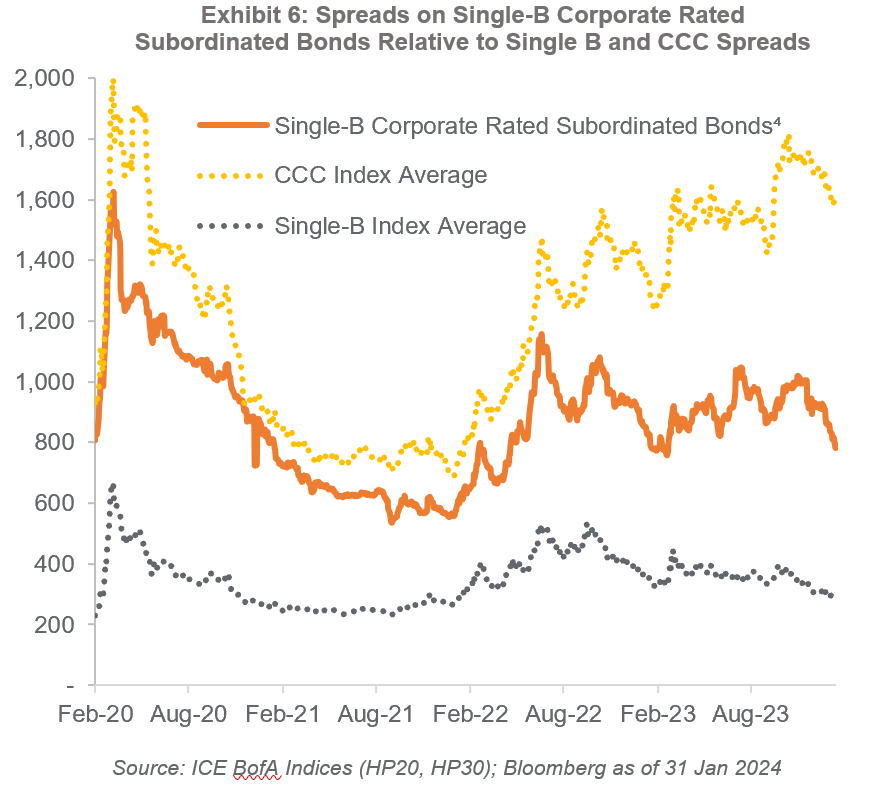

- CCC bonds are at the bottom of the high yield ratings spectrum. Comprising only 5-6% of the relevant European indices, in widening markets, CCCs tend to absorb much of the price dispersion.

- Over the last decade, credit markets have been largely undifferentiated, and European high yield CCCs have not offered good risk reward. However, at current market pricing CCCs offer a yield-to-maturity of 19% and trade at an historically wide premium of more than 1,000 basis points over the single-B credit index.

- Credit ratings are driven by two factors – probability of default and expected recoveries. Within the European CCC universe, Hayfin focuses on the roughly two-thirds of CCC instruments that it believes carry a lower default probability and may offer meaningful positive price convexity.

- Portfolio construction at Hayfin is driven by high conviction and not by benchmark composition. We select securities idiosyncratically, based on sector, credit quality, and price and apply a detailed investment process – combining bottom credit analysis and an active and flexible portfolio framework; thus allowing us to extract interesting risk-adjusted returns within speculatively-rated credit categories.

Corporate bonds and loans rated CCC by S&P or Caa by Moody’s (together “CCCs”) are the lowest rung on the credit quality scale — just above default — and represent high non-payment risk. The rating factors “both the likelihood of default and any financial loss suffered” and is indicative of vulnerability to any adverse conditions1. CCCs today only represent around 5-6% of the European Leveraged Loan and European High Yield Bond indices and are therefore not a core part of the investment universe — furthermore, credit managers may actively aim to minimise exposure to CCCs as part of downside avoidance.

CCCs – a history

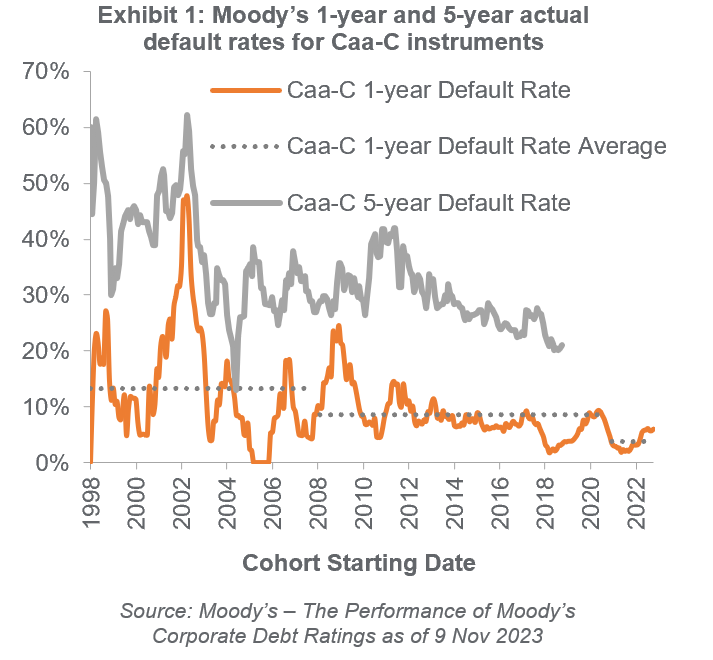

Historically, a large proportion of CCC rated issuers had poor financial or operational momentum which resulted in downgrades from single B to CCC and then default relatively soon after. The complexion of the CCC universe is now markedly different — many CCC instruments have been assigned that rating at issuance rather than being downgraded due to underperformance. This has resulted in a lower default rate for CCCs in the post-Global Financial Crisis era. From 1998-2007, 37% of CCC rated instruments would default within any 5-year period, with peaks of 60% during the Asian financial crisis and the dotcom bubble, and 40% during the Global Financial Crisis and the European Sovereign Crisis. Over the last 5 years that default rate is meaningfully lower at 21%. Similarly, between 1998 and 2007, 13% of CCCs would default in any given 1-year period compared to an average of just 3.7% over the last 24 months.

What is the CCC value proposition today?

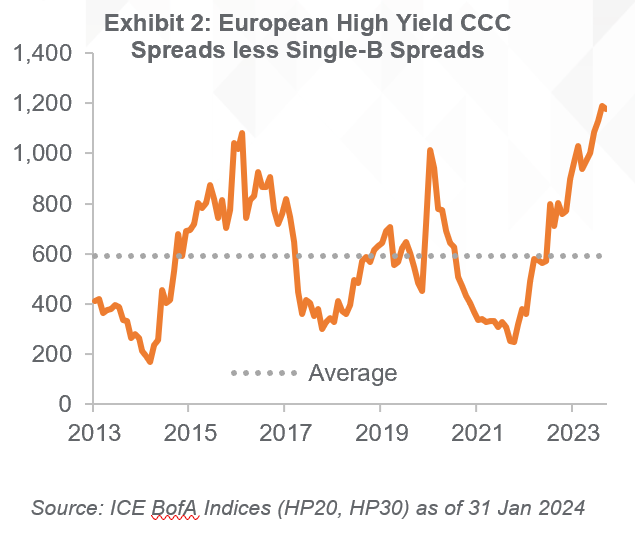

Over the past 10-years2, European CCC high yield as a cohort has delivered an annualised return of 3.0% — below the broader high yield index of 3.5% and the BB-B ratings categories, which have returned 3.6%. Adjusted for volatility, CCCs look even less compelling from an asset allocation point of view. However, the CCC performance differential widened through 2023 and today CCCs are priced at an historically large premium to the rest of the asset class. CCC high yield trades at a spread of 1,600 basis points (bps), which is an unprecedented 1,000 bps premium over Single-B rated high yield — well above the 10-year average spread differential of 592 bps. CCC yield-to-maturity of 19% compares to the broader market at 7%.

The outsized premium for CCCs today warrants the question: is this a compelling time to invest in CCCs, or are we simply being compensated for elevated default losses ahead?

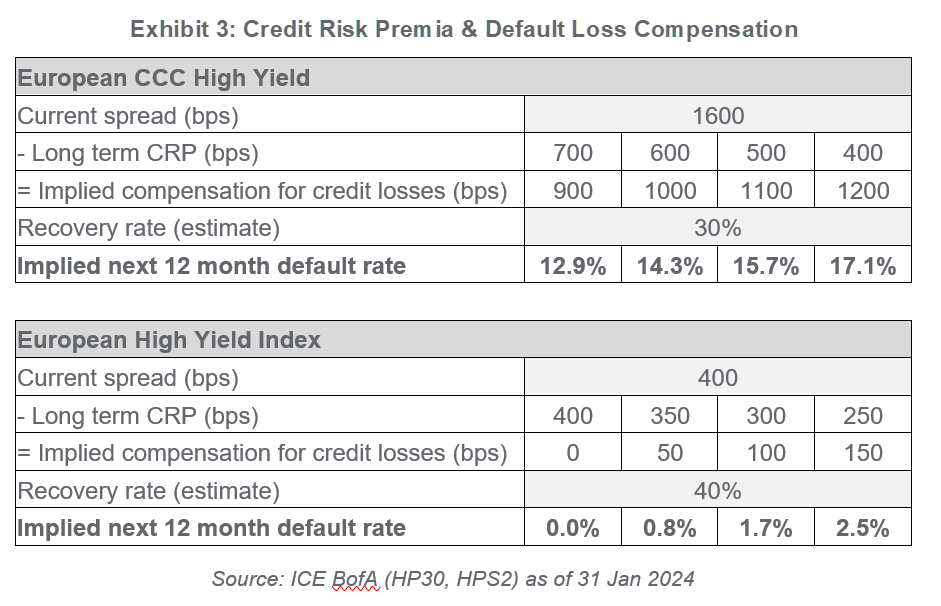

Taking a range of estimates for the long-term credit risk premium (CRP)3 and an assumption on recovery rates, we can impute the compensation for default losses and solve for the default rate priced by the market. Current pricing for CCCs implies a 1-year default rate percentage in the mid-teens, which is much more in line with pre-GFC levels. In contrast, broader high yield index pricing currently implies a low single digit default rate. Current pricing therefore anticipates a meaningful disconnect between the prospects for the CCC cohort as compared to the broader high yield market.

Differentiating within CCCs

Exhibit 4

| Corporate Rating | Security Rating | |

| Single-B | Higher Ranking Debt | Single-B or better (i.e. unchanged or notched up) |

| Lower Ranking Debt | CCC (notched down) | |

We would argue against a broad-brush ‘cohort’ approach to CCCs. Within the CCC universe there is a broad spectrum of credit quality. While some CCCs are the result of credit downgrades of underperforming businesses with unsustainable capital structures, others are of distinctly better credit quality, issued out of companies that have multiple tiers of debt in their capital structure.

Typically rating agencies ‘notch down’ lower ranking debt. Often single-B credit quality corporate issuers will have any lower ranking debt notched down to CCC – reflective of recovery rate rather than prospects of default.

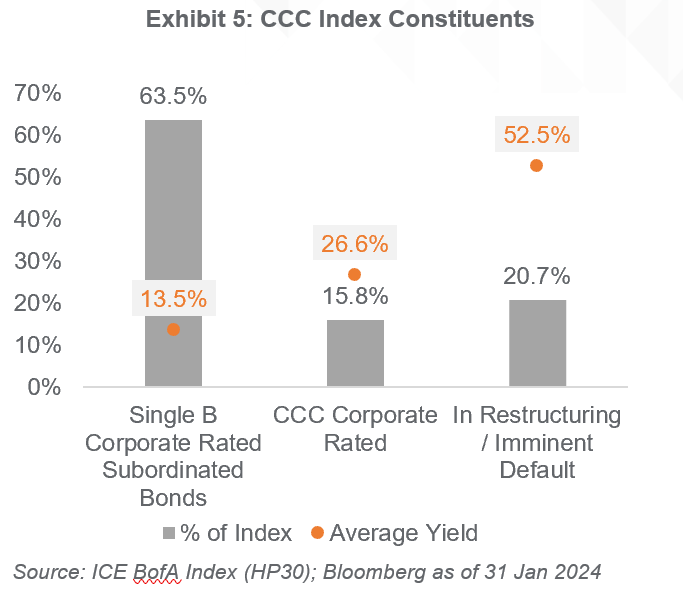

Broadly we can segment CCCs in the European High Yield Index into the following categories, as shown graphically in Exhibit 5, in order of decreasing credit quality:

- Notched down securities with a better corporate credit profile (Single-B or better);

- Securities where both the corporate credit profile and the security profile are CCC-rated; and

- Securities that have defaulted or are imminently expected to default – these securities are much more likely to trade on recovery value (cents on the dollar) where spreads become somewhat meaningless.

Which CCCs can be an attractive risk?

Applying the framework above and reviewing each security in the European high yield CCC universe, we can identify roughly two-thirds of the index as ‘higher credit quality’ (Single-B corporate rating) with lower risk of default. The remaining one-third of the index is made up of lower quality credits with higher risk of default.

The higher-quality issuers still offer a high return without undue risk – these instruments offer an average yield of 13%, which is significantly higher than Single-Bs. Simply buying the whole CCC universe would result in a yield uplift to 19%, however this would mean significantly increasing the risk of defaults within a portfolio.

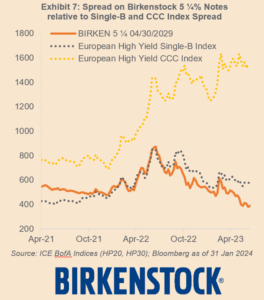

Credit Case Study

In February 2021, L Catterton acquired a majority stake in Birkenstock at a 17x Enterprise Value to EBITDA multiple. Birkenstock manufactures their iconic sandals from a manufacturing base in Germany. To support the acquisition, Birkenstock issued a senior secured EUR term loan (rated B by S&P) through 4.9x net leverage, and a EUR unsecured senior note (rated CCC by S&P) through 6.9x. Despite significant financial flexibility and valuation coverage, the rating agencies notched down the senior notes because of their relative size and low projected recovery in a default scenario.

Ultimately, Birkenstock de-levered rapidly from strong operating performance and cashflow generation and the market overlooked the CCC rating. In fact, the Birkenstock senior notes traded consistently tighter than most single-B rated securities. In July 2023 the notes were upgraded to B- and in November 2023, post-IPO, the issuer rating of Birkenstock was upgraded to BB-, with the notes remaining two notches lower at B.

The job of an investment manager is to identify the best relative value, adjusted for risk — where we are comfortable with the issuer’s competitive positioning, its exposure to the economic cycle, ability to generative positive free cashflow and the sustainability of its capital structure. Ultimately, we must be comfortable that the debt is serviceable and adequately covered from a valuation perspective. Once invested, it is critical to monitor the development of key risks and take appropriate and timely action if the trajectory on these key risks shifts negatively.

In summary, CCCs offer an outsized premium today relative to the history of the asset class. Whilst some of that premium may be required compensation for default losses, there is a significant degree of credit quality differentiation within the CCC cohort. Active and disciplined credit selection is key to delivering attractive risk adjusted returns, isolating the undesirable elements of the benchmark exposure. Hayfin’s current framework emphasises potential for CCCs to add value at market weight where the downside risks can be adequately quantified and managed.

For further information, please reach out to your primary relationship manager or to Investor Relations at IR@hayfin.com.

Sources:

1By the rating agencies, S&P and Moody’s.

2Data to 31 December 2023.

3CRP ranges based on Goldman Sachs estimates, see Goldman Sachs –Global Credit Trader – 8 Jun 23.

4Selected bonds include: Altice International, Banijay, Biogroup, Birkenstock (until upgrade 19/7/2023), Cerba, Foncia, Masmovil, Modulaire, Picard, SFR, TKE, Eviosys, T-Mobile NL, Verisure (until upgrade 15/5/2023), BMC, Ceramtec, Kantar, Kloeckner Pentaplast, Arxada, Merlin, Upfield, Solenis and Tui Cruises. Source: Bloomberg; ICE BAML Indices (HP30, HPS2).

Hayfin today announces that it has signed a contract with Oshima Shipbuilding and Sumisho Marine to construct two new-build 100,000-DWT Post-Panamax dry bulk carrier ships. The vessels, once constructed, will be deliver to an international energy trader on a long-term charter. The project will be funded through Hayfin’s Maritime Yield strategy and underlines the firm’s commitment to the Japanese shipping market, as both an asset-owner and long-term charter provider. The vessels will be managed by Hayfin’s in-house ship management platform, Greenheart Shipping.

The vessels will be constructed at Oshima Shipyard in the Nagasaki Prefecture of south-western Japan and completion is expected to take place within 2026. The vessels will be built to world-leading standards of quality and fuel efficiency, differentiating them from the majority of the current global Panamax fleet that is expected to be non-compliant with International Maritime Organisation sustainability regulations in three years’ time. With just two Japanese shipyards currently building Post-Panamax vessels, contributing to a historically low global orderbook, Hayfin was able to secure these two highly sought-after slots at one of the world’s leading dry bulk specialists through its longstanding relationships with key stakeholders in the Japanese market.

Andreas Povlsen, Head of Maritime at Hayfin, said: “This transaction is another sign of our firm commitment to the Japanese market and demonstrates the kind of attractive asset exposure we can offer to investors through our Maritime Yield strategy; combining fuel-efficient assets and long-term charters to investment-grade counterparties against a supportive long-term market backdrop with consistent tonne-mile growth and a fleet in urgent need of renewal.”

Hayfin recently announced a successful fundraise for its Maritime Yield strategy, equipping the firm with the capacity to acquire $1 billion in shipping assets through equity and debt financing, with a focus on top-specification assets that generate predictable and uncorrelated cash yields from blue-chip counterparties. Having been active in Japan since 2015, Hayfin also opened its Tokyo office last year, led by Tomohiro Hosogaya, the firm’s Head of Japan.

Shipping is a critical component of downstream supply chains, transporting commodities and finished goods valued at over USD20 trillion in 2023.

A strategically important waterway, the Suez Canal (constructed in 1869), reduces travel distances meaningfully. The canal connects the Mediterranean Sea to the Red Sea with approximately 10% of global seaborne trade transiting the Suez Canal and hence the Red Sea.

Over the last few months, tensions in the Middle East have forced trade flow diversions to avoid the Red Sea. This has resulted in expanded tonne miles, increasing asset utilisation rates and has driven up charter rates and dividend yields.

Overview

Whilst Hayfin does not have vessels within its fleet which are scheduled to transit the Red Sea, and we retain the ability in our contracts to reject any request to trade these waters, we expect the current market dynamics of expanding tonne miles and elevated asset utilisation rates to be persistent forces over the medium to longer term.

By exploring the history, geography, and commercial impacts we can better understand real time developments and current and ongoing shift in market dynamics.

Over the last few months, tensions in the Middle East have forced trade flow diversions to avoid the Red Sea expanding tonne miles, increasing asset utilisation rates, and driving up charter rates and dividend yields.

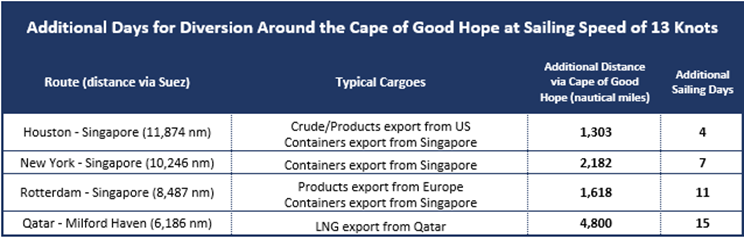

The table below illustrates increased sailing distances and voyage lengths for certain key routes.

At a sailing speed of 13 knots, diversions around the Cape of Good Hope can add up to 15 days in voyage duration, having a knock-on effect on charter rates, insurance premiums and fuel pricing/logistics.

- ‘War risk’ insurance premiums for Red Sea transits have risen by up to 10x.

- Availability of low sulphur fuel oil (‘LSFO’) at key bunkering hubs is a delicate balance; since mid-December 2023 pricing of LSFO in Durban, South Africa has increased 4.0x versus Rotterdam LSFO pricing.

Another consequence of recent disruption is that the proportion of Chinese owned ships transiting the Red Sea has increased significantly i.e. it is ‘western’ ships that are diverting around the Cape of Good Hope, further illustrating the impact of geopolitics in the conflict.

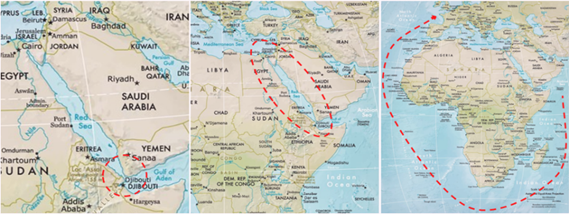

Geography

- Situated between the Arabian Peninsula and East Africa, the Red Sea provides access to Israel’s only port, Eliat, via the Gulf of Aqaba. At the southern end of the Red Sea lies the Bab-el- Mandeb Strait, bordered to the east by Yemen, and both Eritrea and Djibouti to the west.

- At its narrowest point, the Bab-el Mandeb Strait is just 21 miles wide, which is a similar width to the English Channel or approximately 20% of the distance between Florida and Cuba.

- Beyond the Red Sea, lies the Gulf of Aden, bordered by Yemen to the north and Somalia to the south.

Since the hijacking by Houthi militia of the Car Carrier Galaxy Leader (a vessel with links to Israel) on 19th November 2023 in a military operation involving the landing of heavily armed assailants aboard the vessel by helicopter, there have been around 30 attacks against ships transiting through the Red Sea. After what seemed to be an initial focus on vessels with links to Israel or simply calling at Israeli ports, the attacks have seemingly become increasingly sporadic and arbitrary, mostly against ships with no particular nexus to Israel.

As a result of these attacks, the United Nations Security Council has adopted Resolution 272 demanding the Houthis end their attacks and noting “the right of Member States, in accordance with international law, to defend their vessels from attacks.” Consequently, the US and its allies launched Operation Prosperity Guardian, deploying significant naval assets to the region, and launching a series of strikes against land-based targets in Yemen. In retaliation to these actions, the Houthis have shifted focus, attacking ships sailing in the Gulf of Aden off Yemen’s southern coast. This included a missile strike against the Gibraltar Eagle, a Bulk Carrier controlled by US- based Eagle Bulk Shipping, when it was located 90 miles southeast of Aden.

Commercial Impact

The threat posed by these attacks has forced diversions to avoid the Red Sea. Several shipping companies have publicly stated that they will no longer transit the Red Sea.

- It is estimated that since mid-December 2023, Containership arrivals in the Gulf of Arden have fallen 90%, Car Carriers 94%, Tankers 46%, Gas Carriers 86%, and Dry Bulk, least affected, at a 24% decline.

- These diversions also increase the complexity of voyage planning, particularly in terms of sourcing the availability of bunkers (ship fuel). Bunkering is available in South Africa, but supply is limited, and fuel costs are high. For example, as of 18 th January 2024, a metric tonne of LSFO cost USD537 in Rotterdam, USD600 in Singapore, and USD780 in Cape Town.

- The increase in tonne miles has in turn impacted the cost of freight. At the end of September 2023, the Shanghai Composite Containerised Freight Index (the barometer of the seaborne cost of shipping containers from China to global markets) settled at a post-pandemic low of 886.9. By the middle of November, it had risen to 1,000, and has since doubled, reaching 2,206 on 12th January 2024. In product tanker trades, we have seen evidence that spot rates for voyages that would usually pass through the Suez Canal have risen 30-50% since mid-December. Spot rates for long range and medium range product tankers have risen 33% and 29% respectively in the week ending 19th January 2024 alone.

- The southern reaches of the Red Sea have, for some time, been designated a “High Risk Area” for insurance purposes requiring ship owners to pay additional premium for transits. On 18th December 2023, the Joint War Committee at Lloyd’s of London extended the High-Risk Area from 15 degrees to 18 degrees, broadly to encompass the entire lower third of the Red Sea. War risk premiums for Red Sea transits have risen 10x from 0.075% – 0.125% in early December, to 0.5% – 0.75% of the hull value.

- There is also a human impact upon crew members forced to sail in the Red Sea. The crew of both the Galaxy Leader and the St. Nikolas, comprising Ukrainian, Bulgarian, Filipino, Greek, and Mexican nationals are still being held hostage.

Conclusion

Supply chains operate with delicate equilibriums, and delays or disruption tend to increase pricing, benefiting ship owners but perpetuating commodity price inflation.

We have experienced these dynamics several times recently with the trade disruptions during the Covid 19 period, the Suez Canal blockage in 2021 due to the Ever Given, the drought implications in the Panama Canal and the profound impact of shifting energy flows due to the Russia/Ukraine conflict.

The current market dynamics are no different. Since Q4 we have seen increases in the Shanghai Composite Containerised Freight Index by 2.5x. In the same period spot rates on certain refined product tanker trades have increased by up to 50%.

Unlike fixed physical infrastructure, m aritime assets are liquid and dynamic. This is evidenced by shifting trade flows away from the Red Sea and the Suez Canal, instead taking the long route around the Cape of Good Hope as those with interest in ships seek to protect their crews, assets, and cargoes. This drives up freight costs and tightens shipping markets due to increased tonne mile demand.

Persistent trade flow disruptions and expanding ton miles are expected to remain a more permanent feature within supply chains and these market dynamics, on top of healthy long term demand fundamentals, are expected to exacerbate supply/demand imbalances and could likely lead to sharper or longer periods of elevated rates and higher asset yields. When considering these fundamentals against portfolio construction considerations, staggered duration charter contracts across a diversified hard asset base as well as “index-linked” or profit share structures are well positioned to capture these gains and dividend streams.

The kind of interruption to maritime trade that we are currently seeing in the Red Sea has a wide range of ramifications. This includes, first and foremost, the crew members and civilians endangered or otherwise directly impacted by the instability in the region. It also affects consumers and businesses in the form of higher commodity prices and freight costs. But for shipowners and other maritime investors, supply chain disruption can drive up rates and therefore boost yields. This combination of favourable pricing dynamics and a more challenging operating environment looks set to remain a feature of the shipping industry in the medium to long term – layered on top of a longstanding and fundamental supply -demand imbalance that is the primary driver of investor interest in the shipping market.

Hayfin today announces the continued expansion of its global presence having received in-principle approval to open a new representative office in the Dubai International Financial Centre (“DIFC”)*. Through this opening, Hayfin will strengthen its footprint in the Middle East and North Africa (MENA) region.

The expansion underscores the firm’s commitment to growing strategically, following the opening of the Tokyo office at the end of 2023. With an established local presence, Hayfin is set to enhance its coverage in the UAE and Middle Eastern markets and consolidate local investor relationships.

The opening of the DIFC office increases Hayfin’s total number of locations to 13 alongside the firm’s headquarters in London and offices in Frankfurt, Madrid, Milan, Munich, New York, Paris, Luxembourg, San Diego, Singapore, Stockholm and Tokyo. Jack Richardson, Principal, Partner Solutions will be permanently based in the DIFC office and will work under the guidance of Camilla Coriani, Managing Director, Partner Solutions who will oversee efforts in the region.

Alex Wolfman, Global Head of Partner Solutions at Hayfin, said: “The DIFC representative office will form a crucial part of Hayfin’s Partner Solutions approach. The combination of our scale, global footprint as well as depth and breadth of our existing relationships is a solid foundation for us to grow within the region.”

*The Dubai Financial Services Authority approval is subject to Hayfin fulfilling criteria within a six-month period.

Hayfin today announces that it has completed a fundraising process for its Maritime Yield strategy. Having attracted c.$400m in capital commitments for the fund, Hayfin will have the capacity to acquire up to $1bn of shipping assets when coupled with conservative debt financing.

Through the Maritime Yield strategy, Hayfin will invest across each of the industrial maritime sectors, with a focus on acquiring top-specification assets that generate predictable and uncorrelated cash yields from blue-chip counterparties.

Hayfin maintains a discrete profile but has a sizeable Maritime industry footprint with continuous investment activity across direct lending, alternative credit, leasing, and ship ownership, complete with an in-house ship management platform, Greenheart Shipping. This latest fundraising round is a further extension of its track record in the maritime sector, having invested in excess of $3 billion across the various sectors – dry bulk, tankers, containers, LPG, and LNG. The Maritime Yield strategy received strong support from a diverse group of both new and existing investors including leading insurance companies, pension funds, family offices, and infrastructure funds.

Andreas Povlsen, Head of Maritime, commented: “This latest pocket of capital dedicated to the maritime industry is a powerful complement to our existing capabilities. Having acquired more than 80 vessels and concluded more than $1bn of charter revenues, we continue to execute on our strategy of generating strong risk-weighted returns from a quality hard-asset base. Our strategy in maritime focuses on aligning patient institutional capital with attractive fuel-efficient assets and predictable as well as diversified cash yields generated from investment-grade counterparties.”

Nino Mowinckel, Managing Director, Maritime Funds at Hayfin, stated: “Shipping markets are undergoing a period of profound structural change with rising barriers to entry, constrained supply-side dynamics, expanding tonne miles, and tightening regulatory regimes that will increase asset utilisation rates over time. We believe that the industry continues to benefit from adopting a more institutional, value-add infrastructure model, transitioning away from short-termism and sub-scale platforms.”

Njord and Greenheart, a subsidiary of Hayfin Capital Management, have added an extra vessel to their thriving partnership. Njord will design and install a bespoke package of energy-saving devices on the recently bought capesize bulk carrier (to be renamed GH NIGHTINGALE) to boost its performance and commercial tradability. The package will consist of a bespoke combination of technologies, chosen from Njord’s portfolio of more than 30 technologies. They will be installed in dry dock in early 2024, aiming to achieve fuel and emission cuts of between 7 and 16%.

“At Greenheart, improving the performance of our fleet is an integral part of our strategy and so we put each of our vessels on a specific enhancement plan,” says Nikos Benetis, Technical Director at Greenheart Management. “We are pleased that Njord is again able to support us in creating a strong business case for this retrofit. At a time where demand for energy efficiency solutions is high, Njord is able to provide us with very short lead times on buying the energy-saving technology, so we will be able to boost the vessel’s performance and provide an excellent service to our clients from day one. We view our relationship with Njord as a real constructive and trusted partnership.”

The work on GH Nightingale is a continuation of the collaboration between the parties that began in April 2023 when Njord and Greenheart entered into partnership together, along with maritime consulting firm Marsoft. Since then, Njord has designed bespoke packages of fuel-saving technologies for four Greenheart-owned vessels. The scope of the partnership now extends to five vessels, including GH Nightingale. Once the technology is installed, Marsoft will quantify and certify the CO2 savings through carbon credits, ensuring Greenheart is able to optimise the financial value of the fuel savings.

Once the technology is installed, Marsoft will quantify and certify the CO2 savings through carbon credits, ensuring Greenheart is able to optimise the financial value of the fuel savings.

New York – October 26, 2023 – Hayfin Capital Management (“Hayfin”), a leading alternative asset management firm, announces today the expansion of its liquid credit team through the appointment of Peter Swanson as Senior Portfolio Manager and Head of US High-Yield and Syndicated Loans. Peter will be based in New York.

Peter joins Hayfin from Intermediate Capital Group (ICG) where he served as a Portfolio Manager and a Senior Trader investing in syndicated loans and high-yield bonds in CLO and long-only formats. Prior to this, Peter was a Trader at BMO Capital Markets, working on the Leveraged Finance Distribution and Trading team. He brings over a decade of industry experience to the role and will lead the High-Yield & Syndicated Loans team in New York.

Hayfin invests in North American liquid credit assets through its US CLO platform, which manages $2.8bn in AUM across six vehicles. The firm’s US market coverage is complemented by its European High-Yield & Syndicated Loans strategy led by Gina Germano in London.

Peter Swanson, said: “I am excited to join Hayfin at a time when there are attractive return potentials available in North American high-yield credit for those able to navigate uncertain market conditions. The firm has built a high-quality team and a historically robust US CLO platform. I look forward to helping to build on that strong foundation.”

Tim Flynn, Co-founder and Chief Executive Officer at Hayfin, said: “I’m pleased to welcome Peter to the team. His industry experience combined with Hayfin’s dynamic approach in creating effective capital solutions across the credit spectrum puts the firm in a great position. The US remains a critical market with significant opportunities and we have built a great team to capitalize on that.”

Ends

Notes to Editor

About Hayfin Capital Management

Founded in 2009, Hayfin Capital Management (“Hayfin”) is a leading alternative asset management firm with c. €31 billion in assets under management. Hayfin focuses on delivering attractive risk-adjusted returns for its investors across its private debt, liquid credit and private equity solutions businesses.

Hayfin has a diverse international team of over 200 experienced industry professionals with offices globally, including headquarters in London and offices in Frankfurt, Munich, Madrid, Milan, Paris, Luxembourg, Stockholm, New York, San Diego, Singapore and Tokyo.

Further information can be found at hayfin.com.

Contacts:

Hawthorn Advisors: +44 (0)7858 373930

James Davey hayfin@hawthornadvisors.com