2026 is shaping up to be an important year for portfolio financing markets. A mix of macro uncertainty, evolving CLO technicals, and more selective lender behaviour is influencing pricing and terms in ways that Managers will need to navigate carefully.

For Managers running asset-backed lending (ABL) facilities and subscription lines, being well prepared and well positioned can make a meaningful difference in achieving attractive economics. What follows is our current read of the market—where the opportunities sit, where the risks are building, and how we are positioning to stay ahead of both.

Market Context: CLO and ABL Technicals

European CLO markets entered 2026 from a position of meaningful technical strength. A record number of open warehouses, a deep pipeline of reset candidates from 2024 vintages exiting non-call periods, and an increasingly diversified investor base all underpinned a constructive backdrop heading into the year. New issuance expectations for 2026 range from €50bn to €65bn across major bank research desks, and the European market has now grown to over €300bn in outstanding volume, roughly one third the size of its US counterpart.

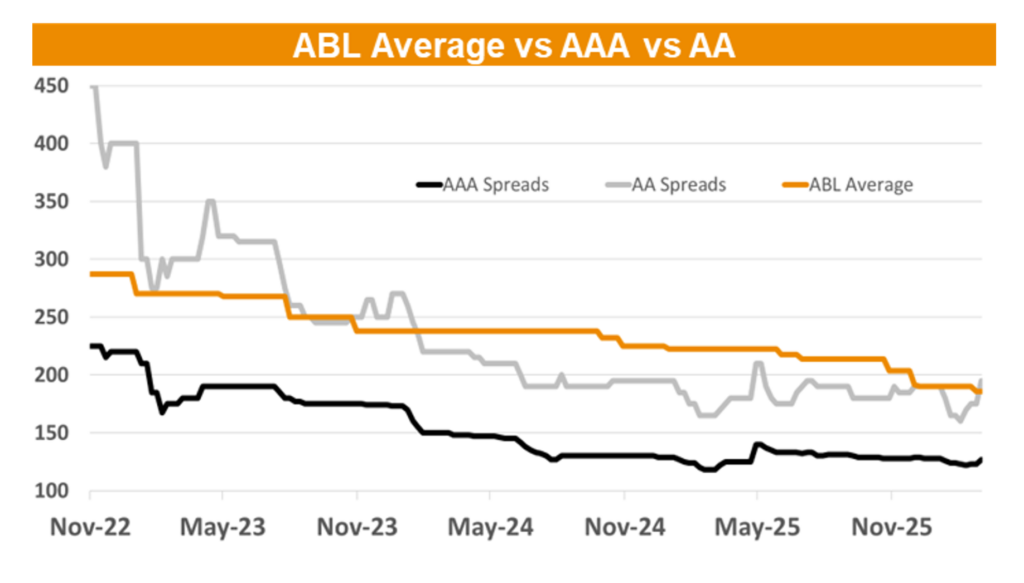

The spread trajectory tells its own story. Average primary AAA coupons on European CLOs peaked at around 191 bps in Q2 2023, tightened to 150 bps by Q1 2024, and compressed further to approximately 132 bps on average through 2025—reaching lows of 119 bps in early February 2026 before geopolitical events intervened (Source: Pitchbook, March 2026). The reset wave was a direct consequence: over €49bn in reset deals were printed in Europe in 2025 alone, versus €30bn in all of 2024, as managers raced to lock in lower liability costs before the window closed.

That window has now narrowed. Following the onset of the Iran conflict and associated risk-off sentiment, AAA primary spreads have widened by around 5–10 bps from their February tights, while BB spreads have moved on average 100–150 bps wider across both European and US markets (Source: Pitchbook, March 2026).

That foundation matters for ABL markets, given ABL pricing does not operate in isolation—it has tracked movements in AAA CLO spreads consistently since late 2022. The tightening cycle compressed the ABL illiquidity premium materially and signalled strong lender appetite throughout 2023–2025. The recent reversal, though modest at the AAA level, has been enough to introduce friction into ABL negotiations. Managers planning upsizes in the near term should expect a more careful conversation with lenders than they would have had three months ago.

Financing Environment: ABL Market Dynamics

The ABL market is where the more complex dynamics are playing out. Sentiment here is increasingly tethered to broader CLO market conditions, and the noise has been amplified by negative headlines across software valuations, ABS structures, BDC performance, and leveraged loan and private credit markets more broadly.

The practical effect has been a sharpening of lender scrutiny. Underwriters are asking harder questions about valuation practices and the performance of underlying assets. Peer repricings are becoming more common. Most financing counterparties remain active and engaged—but conservative or less experienced lenders are tightening covenants or simply pulling back, and the bifurcation in lender quality is becoming more pronounced. Managers who built facilities with inadequate covenants or with weaker counterparties during the tighter-spread environment of 2023–2024 may find those relationships less reliable precisely when they need them most.

For those newer to this corner of the market, it is worth grounding the discussion in the mechanics. ABL financing operates at the SPV level, with facilities secured against a defined pool of assets. Lenders monitor collateral performance closely—tracking covenant headroom, leverage ratios, and, increasingly, the quality and consistency of valuation methodology.

The comparison to CLO structures is instructive. Both use asset-level security and structural protections to give lenders confidence in their risk exposure. The key difference is liquidity: CLOs benefit from a more liquid secondary market, which means the illiquidity premium embedded in ABL pricing has historically reflected that gap. As CLO spreads have tightened, so has that premium—but it has not disappeared, and in periods of stress it can reprice quickly.

The two risks managers need to manage actively are asset underperformance risk—where collateral value declines push LTV ratios toward covenant triggers—and liquidity risk, where stressed lending conditions reduce the availability of financing at precisely the moment it is most needed. Neither risk is theoretical at present.

Optionality Under Stress: Hayfin’s Approach to Today’s Market

We have deliberately invested in building in‑house portfolio financing capabilities—dedicated specialists with long-standing lender relationships. This allows us to operate proactively rather than reactively, identifying which facilities should be secured, refinanced, or renegotiated well ahead of market inflection points. Our team’s technical expertise and continuous market engagement mean our clients benefit from preparedness, not pressure.

A recent example illustrates the value of this approach. One of our banking counterparties proposed mid‑facility adjustments to our valuation framework while preserving the agreed economics. Our ability to engage constructively, grasp the technical nuances, and arrive at a practical solution demonstrated the depth of the team, the strength of our lender relationships and our ability to navigate these discussions effectively to achieve strong outcomes for our clients.

A further pillar of our approach is intentional counterparty diversification. Concentrating ABL facilities with a small number of lenders—however strong those relationships may feel in benign conditions—creates an asymmetric vulnerability: when market sentiment shifts, those who rely heavily on one or two banks find their financing options constrained at exactly the wrong moment.

We have structured our lender base deliberately to avoid that exposure, spreading facilities across a mix of Tier 1 banks, regional lenders, and non‑bank counterparties with differentiated risk appetites and funding bases. The result is a portfolio of financing relationships that does not move in lockstep with any single institution’s internal risk appetite or balance sheet constraints. As parts of the lender market become more cautious, particularly among newer entrants, our diversified network ensures we retain a range of established alternatives and can continue to operate with confidence.

We also run competitive RFP processes systematically when securing or refinancing facilities. In a market where lender appetite is differentiated and pricing is moving, there is no substitute for a proper process to extract best economics. Platform scale matters here—our size and the breadth of our lender relationships ensure we see pricing and structure across a wide cross‑section of the market, not just what any single bank wants to put in front of us.

Perhaps most importantly, deep market participation gives us real‑time intelligence on what peers are experiencing. Knowing that repricings are clearing—and understanding which lenders are driving that activity versus which are retrenching—allows us to calibrate our own negotiations with considerably more precision than relying on market rumour.

The portfolio financing market in 2026 is functioning, but it is far less forgiving. CLO technicals remain broadly supportive, lender appetite is intact, and transactions continue to get done. However, the era of wide lender pools and easily achieved economics has passed for now. Managers who will be best positioned are those who have cultivated strong counterparty relationships, maintained disciplined valuation practices, and built the in‑house expertise and market access to negotiate from a position of genuine insight.

Agility, lender diversification, and data‑driven negotiation have become essential elements of navigating today’s market. At Hayfin, we see preparation as the most effective way to manage financing volatility—staying close to market developments, engaging early with counterparties, and ensuring we approach each discussion with a clear sense of the available options and the right economic outcomes for our clients.