Hayfin today announces the successful close of Hayfin Direct Lending Fund V (“DLF V”), having attracted capital in excess of €15 billion, significantly exceeding its target for the fundraise. The fundraise comprises the commingled Hayfin Direct Lending Fund V, which has reached a final close, together with related investment vehicles. At the time of the close, DLF V had already deployed more than 50% of commitments across over 35 companies.

Through its Direct Lending strategy, Hayfin sources, structures and invests in performing senior‑secured loans to primarily European middle‑market and upper‑middle‑market businesses, with an emphasis on downside protection and robust cash flow generation or asset coverage. The vast majority of these loans are originated through an extensive relationship-based primary sourcing network spanning 13 offices and dedicated sector‑specialist teams. This broad-based origination model has allowed Hayfin to build a diverse portfolio of loans to a wide range of cash‑generative businesses, with minimal exposure to software credits deemed most susceptible to AI disruption. Hayfin invested a record €7.1 billion into Direct Lending transactions in the last twelve months, bringing total strategy deployment to over €38 billion across more than 350 investments since the firm’s inception.

The fundraise attracted capital commitments exclusively from a global institutional investor base, comprising public and private pension funds, financial institutions, insurance companies, sovereign wealth funds, funds of funds, endowments, consultants and family offices. Recent strains within semi-liquid US private credit funds for retail investors have accelerated LP demand for conservative fund structures, in line with Hayfin’s approach of securing locked-up capital in closed-ended drawdown and institutional evergreen vehicles. This helped Hayfin to achieve the most significant milestone yet for its flagship private credit strategy with the successful close of Direct Lending Fund V, more than doubling the amount raised for Direct Lending Fund IV, which closed in August 2023 with over €6bn in total commitments.

The DLF V fundraise also includes the successful close of a rated note feeder which contributed approximately $600 million of total investable capital. The structure, advised on by Proskauer as Legal Counsel, provides insurers with capital-efficient access to Hayfin’s European Direct Lending strategy, reflecting the firm’s commitment to broadening access to its private credit platform across a diverse range of institutional investor types.

Mark Tognolini, Co-Chief Executive Officer and Co‑Founder of Hayfin, commented: “We are very pleased with the successful close of Direct Lending Fund V and grateful for the strong support from both new and long‑standing investors. At a time when parts of the private credit market are experiencing heightened volatility, this fundraise reflects confidence in our disciplined underwriting, our highly specialised team, our conservative approach to fund structuring and our differentiated origination model, which has been built to perform consistently across market cycles.

“In recent months, longstanding differences between the US and European private credit markets have become even more pronounced, with European lenders continuing to benefit from greater market fragmentation, continued bank retrenchment and a predominantly institutional capital base. Against this backdrop, we are well placed to take further market share and support high‑quality European businesses with flexible financing solutions – as we have consistently done in other periods of volatility – while preserving our focus on capital preservation and downside protection.”

Hayfin was advised on the fundraise by Macfarlanes.

Since it was founded in 2009, Hayfin has invested over €55bn of capital across more than 500 portfolio companies via its private credit strategies.

Hayfin has fully underwritten the debt financing to support the acquisition of Hyve Group (“Hyve”), a leading next-generation B2B events business, by Hellman & Friedman (“H&F”). H&F is acquiring Hyve from Providence Equity Partners (“Providence”) and Searchlight Capital Partners (“Searchlight”), marking the next phase of Hyve’s growth and evolution.

The senior-secured facility extends an existing lending relationship with Hyve. Hayfin first invested in the business in 2021 and then again in 2023 when supporting its take-private by Providence and Searchlight. Since then, Hyve has delivered three consecutive years of double-digit organic revenue growth, expanded EBITDA beyond $100m and built out its platform through seven strategic acquisitions and five key event launches, while investing significantly in technology and tech-enabled products and services. In partnership with H&F, Hyve will focus on accelerating international launches, expanding adjacent products and services and continuing to scale into growing end markets via its proven acquisition strategy.

Founded in 1991 and headquartered in London, Hyve operates a global portfolio of premium, must-attend B2B events connecting some of the world’s leading companies, investors, innovators and decision-makers. It operates across high growth sectors such as healthcare, ecommerce, edtech, supply chain and martech, with flagship events including HLTH, Shoptalk, Bett, Mining Indaba and Fintech Meetup. Under its current leadership team, Hyve has positioned itself as a partner platform of choice for ecosystem events in high growth markets, with a customer offering spanning content, intelligence, matchmaking and membership.

Stuart Mitchell, Director at Hayfin said: “Having first invested in Hyve in 2021, including in its most recent ownership by Providence and Searchlight, Hayfin has developed a deep understanding of the business and its exceptional growth record. During this period, Hyve has transformed into a more global, diversified and digitally sophisticated platform, with strong momentum behind it. We look forward to working with Mark and his talented team as they enter this exciting next phase of the company’s development in partnership with H&F.”

Rehan Jiwani, Managing Director at Hayfin said: “We have been lenders in the B2B events space for more than 15 years and we have on-going strong conviction in the attractiveness of the sector. Hyve is an example of an exceptionally strong platform within B2B events, and we are excited to support the company with this latest, large-scale, financing. From a Hayfin perspective, it highlights our ability to provide sizeable financing solutions that support sponsors and management teams in executing their growth ambitions.”

Completion of the transaction is expected by the end of the calendar year.

Last month, we welcomed over 90 investors, partners, and colleagues to 10 Grand Central for what turned out to be a truly memorable day. The world had intervened in the weeks before in a way that gave every conversation an urgency and an honesty that can be hard to manufacture in a well-rehearsed agenda.

But the event really started the evening before when we hosted a dinner for a group of our limited partners – a deliberately smaller, less structured setting than what was to follow. No presentations, no panels. Just conversation. We wanted to hear directly from investors: what was on their minds, what was worrying them, what they needed from us that we weren’t yet delivering. The conversations that evening were candid in a way that only happens when there’s no agenda. They shaped the morning that followed, with three themes – portfolio transparency, views on AI disruption across our own portfolios, and the durability of European private credit – resurfacing in a more structured form throughout the day.

Our co-CEO Mark Tognolini opened the day and has written here about what’s been at the forefront of his mind in the opening months of the year. Let me give you a sense of what emerged – not panel by panel, but as the through-lines I kept coming back to across a genuinely substantive day.

The second-order effects are the underpriced story

After an opening session on the shifting macroeconomic environment, Jeff Currie picked up the threads from Andrew Sheets’ earlier framing and set out a clear way to think about commodities: physical markets clear today’s supply and demand, while financial markets price the future. The gap between the two – Brent at $120 in the physical market versus the low 80s in futures markets at the time – was not a rounding error. Markets were pricing a rapid resolution that did not square with the physical reality of bringing supply back on line; closed wells take months or years to reopen, not days.

What struck me wasn’t the headline oil disruption—that story was everywhere—but the second-order effects that rarely make the front pages. Nino Mowinckel walked through the specifics: over half of global seaborne sulphur trade transits the Strait of Hormuz, putting copper and nickel production at risk. Indonesia, the world’s largest nickel producer, imports around 75% of its sulphur from the Persian Gulf. Around a fifth of global refined copper output depends on sulphuric acid, while 24% of global fertiliser supply remained stuck behind the Strait. The inflationary impact may not show up until the second half, long after the headlines move on.

“The edge in European private markets is not price or leverage; it is the compounding advantage of being present in the right relationships for long enough that complexity becomes a differentiator, not a deterrent.”

Jeff Currie, formerly at Goldman Sachs and now running Energy Pathways at Carlyle, put a structural lens on it: the world that prioritised affordability and environmental credentials above energy security has been forced to reorder its priorities. His broader rotation thesis – from asset-light to asset-heavy, the “HALO” trade – felt less like an acronym and more like a description of what we have been quietly building for over a decade.

Complexity is a feature of our market, not a problem – if you’ve built for it

The edge in European private markets is not price or leverage; it is the compounding advantage of being present in the right relationships for long enough that complexity becomes a differentiator, not a deterrent.

40% of our Direct Lending book is originated through sole lender deals; the rest are typically clubs of two to three lenders. Stephen Badia’s argument was that European private credit still looks far more like an extension of banking than a convergence with the syndicated market, and that inefficiency can be both a structural return driver and risk mitigant. Rehan Jiwani quantified it: a clear premium available in Europe versus comparable US credits – alongside lower leverage, tighter documentation and smaller syndicates that preserve genuine lender control.

Healthcare, Maritime and Real Estate showed the same dynamic in specialist form. Andrew Merrill made the case that our platform generates continuous opportunities to finance a company across its lifecycle and that even transactions we have declined can build an edge in the future. Over several years, the Healthcare team reviewed three plasma product businesses across the EU and the US, which for various reasons did not result in an investment; instead, it set the stage for a future successful investment in the space. Hayfin underwrote an FDA-inspected plasma manufacturing plant that was still loss-making as it restarted post-shutdown – conviction built through years of accumulated diligence.

Hayfin’s Greenheart Management, our wholly owned ship management subsidiary, is the Maritime equivalent. There we have operational directors tracking fuel consumption per knot across every vessel. That operational credibility is what earns 5–20-year contracts from investment-grade counterparties. Duration requires trust, and trust is built through cycles, not just sharp terms on the day.

As punctuated by Carlos Colomer, within real estate markets, the difference between partnering and not often comes down to local presence and cultural nuance. We understand how an owner thinks about control, how they weigh optionality, and how they want a structure explained. We meet people where they are—literally and figuratively—and communicate terms in a way that feels natural and precise. In relationship-driven markets, that is not a detail.

The private credit stress is real, but the systemic risk framing is wrong

The “Private Credit at a Crossroads” panel met the questions LPs are rightly asking. The backdrop is tough – the weakest quarter for direct lending fundraising in three years; BDCs trading at a discount to NAV – and the panel didn’t pretend otherwise.

Carlos Pla drew a key line: the semi-liquid vehicles under the spotlight are roughly a quarter of a now $2 trillion+ global private credit market, with average leverage around 1.2x – figures that were dwarfed by the embedded risks that defined the pre-GFC banking market. The other three-quarters of assets sit in closed-end funds, structures built for patient, disciplined deployment designed to take advantage when others pull back. Our €7 billion of undrawn capital is the practical expression of that design.

Michaela Campbell pushed back on defaults as the headline metric: they are backward-looking, inconsistently defined across managers and often deferred through amendments. The better litmus is in leading indicators – interest coverage trajectories, PIK toggle usage, watchlist trends and amendment volumes. On those measures, Hayfin’s Direct Lending portfolio looks considerably healthier than the headlines. The watchlist has fallen by almost a third since YE-2023; weighted average interest coverage ratios remain stable across consecutive quarters; and the vast majority of interest remains cash-paid.

On AI disruption, our underwriting framework extends well beyond software. As Mark Bickerstaffe put it, every sector we lend into is subject to the same question: what are the second-order effects if AI changes the economics of the profession or sector this business serves? We take a “guilty until proven innocent” approach to each company’s resilience to AI risk. There are no clean answers yet – which argues for caution in exposed sectors, not urgency. Marc Chowrimootoo made a related point on fraud: the headline cases have been non-sponsored, inventory-backed trades, and fraud is not a private credit phenomenon so much as a human one. The discipline is screening bad actors before you lend, including walking away when terms look good, but the governance does not.

“The illiquidity in private markets is an opportunity, not just a problem.”

The afternoon session on illiquidity could have been a sobering inventory – significant inventory of legacy assets seeking an exit and average hold periods stretching out fund terms. Instead, it showed how flexible, patient capital, in the form of either credit or equity, can step in where the market has no ready solution. The toolkit across private markets is broader than many assume: dividend recaps, bridge-to-IPO financing, continuation vehicle support, minority stake buyouts and management-led buyouts of the sponsor itself.

Sponsors are increasingly reluctant to sell their best assets — and our Private Equity Solutions Strategy is built around that reality. As Vladimir Balchev put it, the priority is less about DPI than TVPI: sponsors want solutions that extend hold periods and build value, not just accelerate distributions. In the small and mid-cap segment especially, the constraint is not liquidity for star assets – it is time and growth capital. GP-led transactions are now a core tool for addressing both, not a last resort.

A consistent origination edge permeated the discussion: relationships built over years, portfolios mapped 12 to 18 months before a transaction and credibility earned through repeat execution. For many mid-market sponsors, the choice is simple: they back partners who have been in the room before, not those who show up only when the process starts.

On listening

In closing, Tim Flynn left the audience with a simple wish: that if investors take one thing away from Hayfin, it is that the firm is built to deliver client outcomes regardless of where we are in the cycle.

Tim’s framing connected directly to how the day had started, and to the dinner the evening before. We are deliberate about listening, creating an environment in which investors can tell us what they need, rather than simply what we had come prepared to tell them. That commitment is what made the panels as honest as they were about the challenges facing the asset class. Honesty of that kind is either native to a culture, or it isn’t. You cannot manufacture it for an investor day and quietly retire it on the way home.

Thank you again to everyone who joined us in New York. Your continued partnership genuinely matters to us.

Hayfin has secured initial capital commitments to support the growth of its European CLO business, as part of a broader initiative to deepen its European alternative credit capabilities and scale the Hayfin platform.

Hayfin has a long and established track record in European CLOs, currently managing €5.8 billion in assets across 14 transactions, following the completion of four successful resets in 2025. These latest capital commitments will support continued growth in the platform by providing equity for future European CLOs issued and managed by Hayfin.

As part of this renewed strategic focus on its core European investing businesses, Hayfin has decided to appoint Greensledge as an advisor to explore options for its US CLO business, which represents €1.4 billion of assets under management. The US CLO platform has historically performed strongly, supported by disciplined underwriting and rigorous credit processes, and the firm is committed to an orderly process that protects the interests of noteholders and other investors.

Mark Tognolini, Co-Founder & Co-CEO of Hayfin Capital Management, said: “We are excited to announce this latest capital raise which supports the continued growth of our European platform, particularly in light of the significant opportunity we see as an established player within European liquid credit. With a strong team and experienced leadership in place, we are confident in our ability to execute with discipline and a continued focus on clients.

“The US CLO team has a strong historical track record and we are committed to ensuring continuity for investors throughout this process. We will work closely with the team and Greensledge to identify the best outcome for all stakeholders.”

When preparing to host Hayfin’s North American clients at our annual US AGM in New York last month, we knew three topics would be at the forefront of their thinking: software, retail redemptions and the Iran conflict. The discussion became a timely test of how private credit managers can demonstrate that they are the right partners to help investors navigate market volatility.

New AI models have triggered a repricing of business durability in the face of accelerating disruption, prompting LPs to examine their GPs’ exposure to potential losses in software, where private credit is often seen as heavily concentrated. At the same time, a surge in redemptions and gating in some US semi-liquid private credit vehicles has forced price discovery and raised the prospect of supply shocks. Finally, despite the fragile ceasefire reached in April, tensions in the Middle East continue to ripple through supply chains, commodities pricing and energy markets.

These three trends are playing out differently on either side of the Atlantic. In the case of the first two, the impact should in theory be more muted in Europe. Software is a smaller part of European lending than in the US, where it accounts for an estimated 20–25% of private credit activity. In Europe, higher-risk ARR lending to pre-profit software businesses with unclear paths to deleveraging is far less prevalent. Similarly, while retail capital has grown to 20–25% of global private credit AUM, withdrawals have been concentrated in US Business Development Company (BDC) and interval fund structures rather than in European vehicles, which are still relatively nascent.

But Europe is unquestionably more exposed to geopolitical risk – at least from the specific perspective of disruptions to energy supply and the resulting increase in inflation.

Is your money safe?

In all three cases, the first question that LPs should be asking their private credit managers is how they will preserve capital, protect value and limit downside risk within their existing portfolios.

We have previously explained why we remain underweight software across both our Private Credit and High-Yield & Syndicated Loans businesses. Our software exposure across Direct Lending portfolios is less than 6%, and below 5% in our latest vintage, which compares favourably with peers.

We have managed that exposure through prudent portfolio diversification and a clear view that software is not only potentially vulnerable to generative AI disruption, but also one of the most competitive parts of the market. Where we are invested, those loans are to large, mature, high-growth companies backed by sector specialist GPs. We have grounded our credit judgment in traditional credit metrics rather than uncertain enterprise value assumptions.

Uncertainty is not an environment we are waiting to pass. It is the environment we are built for.

We are similarly well placed on liquidity. Hayfin’s private credit strategies rely exclusively on fully locked-up institutional drawdown funds, with no retail capital. We had already been seeing growing demand for institutional vintage solutions that operate as drawdown vehicles, with redemptions achieved through natural portfolio run-off rather than forced asset sales. That trend now looks set to accelerate.

No manager, least of all one investing in Europe, can be fully insulated from the effects of conflict involving Iran. We saw during Covid and in the early stages of the war in Ukraine how shocks to energy, transport and agricultural supply chains can quickly spread through interconnected markets. Higher energy, fertiliser and freight costs would feed into food prices and create broader inflationary pressure.

Our dedicated Maritime team, with 15 industry specialists, more than $4 billion deployed and over 100 vessels acquired, gives us added insight into how global supply chains are being affected.

Where can managers create an edge?

The second question LPs should ask their GPs is how they are positioned to capitalise on these market dislocations. Throughout Hayfin’s history, periods like these have created the conditions for us to grow, gain market share, deepen relationships with borrowers and LPs, and deliver some of our best-performing investment vintages. Uncertainty is not an environment we are waiting to pass. It is the environment we are built for.

The obvious counterargument is that the private credit industry as a whole tends to gain market share from banks and syndicated markets during periods of disruption. The more important question, then, is what positions us to deliver compelling investment returns in a more uncertain environment relative to our competitors.

Our European focus is certainly an advantage. We consider ourselves the European home team, with 17 years of track record and a platform built to operate across fragmented jurisdictions, languages and legal regimes. The distinctive, longstanding opportunity set in Europe, as we have previously discussed, certainly still applies. There remains room for further growth, with the UK and EU’s combined GDP totaling 90% of the US, but with private markets just one third of the size. Additionally, as a shallower market than the US, Europe can reprice quicker in environments like this.

Hayfin’s adaptability and ‘one-firm’ culture, both of which I described earlier this year, are also well-suited for the current landscape. Our broad set of complementary strategies allows us to finance both growth and stress, and to lean into the parts of the market offering the best risk-adjusted returns, as this rapidly shifts around us. By operating in a de-siloed, integrated manner, when markets “flash amber”, we draw on the insights and experience of the whole team to re‑underwrite portfolios, reassess risks and recalibrate pipelines.

Recent market stresses will also affect future investment vintages. One potential second‑order effect of the recent strains in US private credit is that both LPs and borrowers will increasingly favour managers with more conservative approaches to fund structuring. US lenders might pull back from European markets, tipping competitive dynamics in favour of homegrown European managers with more institutional capital.

Patient capital – at scale

Many of the themes discussed here are only beginning to play out. We will remain patient, focusing first on supporting our existing borrowers as the market comes to us.

At the same time, we are preparing to invest selectively through our Tactical Solutions, Special Opportunities and Private Equity Solutions strategies. In these areas, choppier markets and a rising tide of €300 billion in net asset value without sponsor capital support are likely to drive demand for hybrid liquidity solutions.

With a significant undrawn capital position of c. €7bn today, we have the scale and firepower to capitalise on the opportunities that may present themselves in the months ahead.

Hayfin is pleased to announce that it acted as sole lender in providing the debt financing to support Axcel’s acquisition of Geomatikk from Hg.

Geomatikk is a Norway-based provider of mission-critical tech-enabled services for the management and protection of critical infrastructure. Its integrated offering allows for full value chain coverage and underpins significant value-add for infrastructure stakeholders, including network operators, excavators and municipalities. The group has operations in Norway, Sweden and Finland, and recently expanded to Denmark and Spain.

The transaction will enable Geomatikk to cement its leadership in the Nordics and pursue further expansion across other European markets.

Marco Ferrari, Managing Director, Private Credit, commented: “Geomatikk is an established market leader in an attractive and resilient niche, well-entrenched within an ecosystem which it helped build. We are excited to partner with Axcel and the management team, and to support the next chapter of the company’s growth journey. The transaction reflects Hayfin’s commitment to the Nordic region, where we see interesting opportunities for our Private Credit strategy.”

2026 is shaping up to be an important year for portfolio financing markets. A mix of macro uncertainty, evolving CLO technicals, and more selective lender behaviour is influencing pricing and terms in ways that Managers will need to navigate carefully.

For Managers running asset-backed lending (ABL) facilities and subscription lines, being well prepared and well positioned can make a meaningful difference in achieving attractive economics. What follows is our current read of the market—where the opportunities sit, where the risks are building, and how we are positioning to stay ahead of both.

Market Context: CLO and ABL Technicals

European CLO markets entered 2026 from a position of meaningful technical strength. A record number of open warehouses, a deep pipeline of reset candidates from 2024 vintages exiting non-call periods, and an increasingly diversified investor base all underpinned a constructive backdrop heading into the year. New issuance expectations for 2026 range from €50bn to €65bn across major bank research desks, and the European market has now grown to over €300bn in outstanding volume, roughly one third the size of its US counterpart.

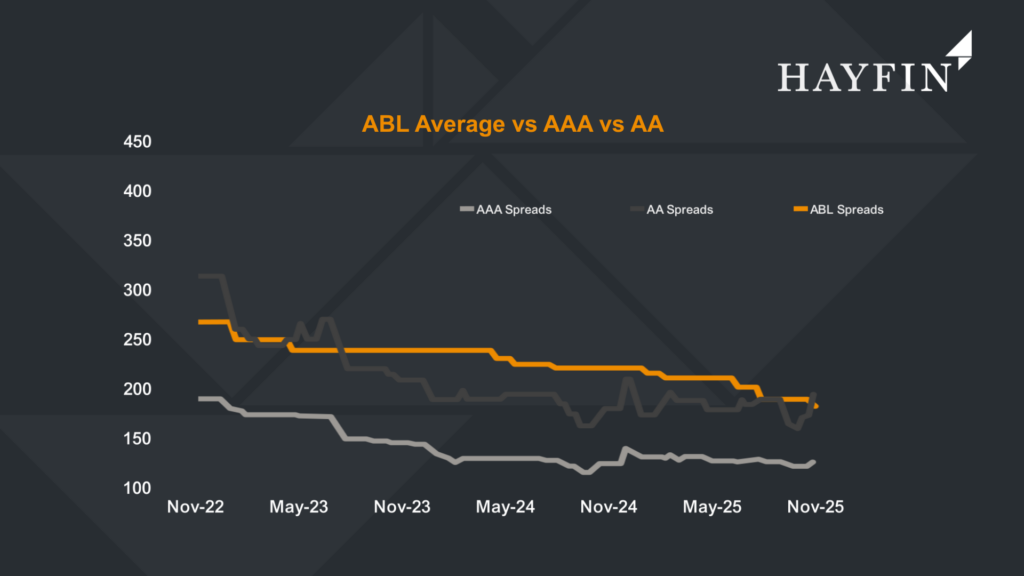

The spread trajectory tells its own story. Average primary AAA coupons on European CLOs peaked at around 191 bps in Q2 2023, tightened to 150 bps by Q1 2024, and compressed further to approximately 132 bps on average through 2025—reaching lows of 119 bps in early February 2026 before geopolitical events intervened (Source: Pitchbook, March 2026). The reset wave was a direct consequence: over €49bn in reset deals were printed in Europe in 2025 alone, versus €30bn in all of 2024, as managers raced to lock in lower liability costs before the window closed.

That window has now narrowed. Following the onset of the Iran conflict and associated risk-off sentiment, AAA primary spreads have widened by around 5–10 bps from their February tights, while BB spreads have moved on average 100–150 bps wider across both European and US markets (Source: Pitchbook, March 2026).

That foundation matters for ABL markets, given ABL pricing does not operate in isolation—it has tracked movements in AAA CLO spreads consistently since late 2022. The tightening cycle compressed the ABL illiquidity premium materially and signalled strong lender appetite throughout 2023–2025. The recent reversal, though modest at the AAA level, has been enough to introduce friction into ABL negotiations. Managers planning upsizes in the near term should expect a more careful conversation with lenders than they would have had three months ago.

Financing Environment: ABL Market Dynamics

The ABL market is where the more complex dynamics are playing out. Sentiment here is increasingly tethered to broader CLO market conditions, and the noise has been amplified by negative headlines across software valuations, ABS structures, BDC performance, and leveraged loan and private credit markets more broadly.

The practical effect has been a sharpening of lender scrutiny. Underwriters are asking harder questions about valuation practices and the performance of underlying assets. Peer repricings are becoming more common. Most financing counterparties remain active and engaged—but conservative or less experienced lenders are tightening covenants or simply pulling back, and the bifurcation in lender quality is becoming more pronounced. Managers who built facilities with inadequate covenants or with weaker counterparties during the tighter-spread environment of 2023–2024 may find those relationships less reliable precisely when they need them most.

For those newer to this corner of the market, it is worth grounding the discussion in the mechanics. ABL financing operates at the SPV level, with facilities secured against a defined pool of assets. Lenders monitor collateral performance closely—tracking covenant headroom, leverage ratios, and, increasingly, the quality and consistency of valuation methodology.

The comparison to CLO structures is instructive. Both use asset-level security and structural protections to give lenders confidence in their risk exposure. The key difference is liquidity: CLOs benefit from a more liquid secondary market, which means the illiquidity premium embedded in ABL pricing has historically reflected that gap. As CLO spreads have tightened, so has that premium—but it has not disappeared, and in periods of stress it can reprice quickly.

The two risks managers need to manage actively are asset underperformance risk—where collateral value declines push LTV ratios toward covenant triggers—and liquidity risk, where stressed lending conditions reduce the availability of financing at precisely the moment it is most needed. Neither risk is theoretical at present.

Optionality Under Stress: Hayfin’s Approach to Today’s Market

We have deliberately invested in building in‑house portfolio financing capabilities—dedicated specialists with long-standing lender relationships. This allows us to operate proactively rather than reactively, identifying which facilities should be secured, refinanced, or renegotiated well ahead of market inflection points. Our team’s technical expertise and continuous market engagement mean our clients benefit from preparedness, not pressure.

A recent example illustrates the value of this approach. One of our banking counterparties proposed mid‑facility adjustments to our valuation framework while preserving the agreed economics. Our ability to engage constructively, grasp the technical nuances, and arrive at a practical solution demonstrated the depth of the team, the strength of our lender relationships and our ability to navigate these discussions effectively to achieve strong outcomes for our clients.

A further pillar of our approach is intentional counterparty diversification. Concentrating ABL facilities with a small number of lenders—however strong those relationships may feel in benign conditions—creates an asymmetric vulnerability: when market sentiment shifts, those who rely heavily on one or two banks find their financing options constrained at exactly the wrong moment.

We have structured our lender base deliberately to avoid that exposure, spreading facilities across a mix of Tier 1 banks, regional lenders, and non‑bank counterparties with differentiated risk appetites and funding bases. The result is a portfolio of financing relationships that does not move in lockstep with any single institution’s internal risk appetite or balance sheet constraints. As parts of the lender market become more cautious, particularly among newer entrants, our diversified network ensures we retain a range of established alternatives and can continue to operate with confidence.

We also run competitive RFP processes systematically when securing or refinancing facilities. In a market where lender appetite is differentiated and pricing is moving, there is no substitute for a proper process to extract best economics. Platform scale matters here—our size and the breadth of our lender relationships ensure we see pricing and structure across a wide cross‑section of the market, not just what any single bank wants to put in front of us.

Perhaps most importantly, deep market participation gives us real‑time intelligence on what peers are experiencing. Knowing that repricings are clearing—and understanding which lenders are driving that activity versus which are retrenching—allows us to calibrate our own negotiations with considerably more precision than relying on market rumour.

The portfolio financing market in 2026 is functioning, but it is far less forgiving. CLO technicals remain broadly supportive, lender appetite is intact, and transactions continue to get done. However, the era of wide lender pools and easily achieved economics has passed for now. Managers who will be best positioned are those who have cultivated strong counterparty relationships, maintained disciplined valuation practices, and built the in‑house expertise and market access to negotiate from a position of genuine insight.

Agility, lender diversification, and data‑driven negotiation have become essential elements of navigating today’s market. At Hayfin, we see preparation as the most effective way to manage financing volatility—staying close to market developments, engaging early with counterparties, and ensuring we approach each discussion with a clear sense of the available options and the right economic outcomes for our clients.

Each year, International Women’s Day offers a moment for corporates, governments and individuals globally to take stock. It provides the opportunity to celebrate progress but also reflect on challenges that still lie ahead.

The pace of change remains gradual. In the UK, women who work full-time still earn on average 6.9% less than men working the same number of hours, although the gap has narrowed by over a quarter over the past decade. In the United States, according to the Pew Research Center, women earn roughly 85 cents for every dollar earned by men, compared with 81 cents in 2003. These trends highlight that while we are moving in the right direction, meaningful progress requires sustained effort.

This year’s theme, Give to Gain, captured that dynamic clearly: meaningful progress comes when organisations actively invest in inclusion, opportunity and leadership development. When businesses create conditions for women to thrive, the benefits extend far beyond individuals; it shapes culture and supports long-term growth.

Against this backdrop, Hayfin’s Global Women’s Initiative hosted its third annual International Women’s Day event, From Retention to Leadership: An International Women’s Day Conversation. Bringing together senior leaders from across the industry, the panel discussion and Q&A explored how organisations can move beyond recognition towards action, such as removing bias in decision-making to expanding opportunities and building stronger leadership pipelines for women.

I was delighted to moderate this discussion, and would like to extend a huge thank you to our panellists: Sharon Bell, Senior Strategist in Goldman Sachs Research; Sabrina Fox, Founder, Fox Legal Training & Good Girl to Goddess; and Maria Johannessen, Head of UK Investment, Aon. Here are some of the key takeaways from the conversation:

Progress demands energy

Driving societal change does not happen overnight, and while systemic issues such as pay gaps are still evident, there has been progress. Representation is gradually improving: women now hold roughly 40% of board roles in FTSE 350 companies, up from 9.5% in 2011, reflecting sustained efforts to strengthen diversity in leadership.

The growing presence of women in senior roles sends an important signal to the next generation that leadership pathways are widening. However, accelerating progress will require continued energy and commitment from businesses and policymakers alike. For corporates, this means moving beyond intent to action – not just actively celebrating initiatives such as International Women’s Day, but also championing female leaders and implementing policies that develop and retain the next generation of talent.

Government also has an important role to play. While legislation such as the Equal Pay Act established an essential foundation, further progress will depend on policies that better support career continuity, including more balanced approaches to parental leave and greater recognition of the realities of time spent out of the workforce.

Sponsorship matters

Another theme that emerged from the discussion was the importance of sponsorship. Having someone advocate for you in meaningful ways when you are not in the room can be transformative. Unlike mentorship, which typically focuses on guidance and advice, sponsorship involves advocacy. A sponsor not only helps individuals clarify their goals and build confidence, but also uses their own influence to create opportunities, promote achievements and support progression into more senior roles.

For many women, a persistent challenge in the workplace is navigating expectations around leadership style. They are often encouraged to be more assertive, more vocal or more confident – yet when those behaviours are demonstrated, they can sometimes be interpreted differently than they would be for male counterparts. Sponsorship can help bridge this gap. By advocating for talent and ensuring contributions are recognised in decision-making forums, sponsors can help counter bias and ensure capability is evaluated fairly.

Models make a difference

Leadership is not only about setting strategy. It is about modelling the behaviours that shape workplace culture. That includes demonstrating that balance and boundaries are both respected and realistic. When senior leaders, both men and women, visibly prioritise responsibilities outside of work, such as leaving the office to pick up children or avoiding a culture of late-night emails and instant responses, it sends a powerful signal about what is truly prioritised within an organisation.

This is particularly important when considering the unequal distribution of unpaid work. Data from the Organisation for Economic Co-operation and Development (OECD) shows that women globally do almost 50% more unpaid domestic and care work than men. When a significant proportion of time outside the workplace is already committed, expectations around constant availability can disproportionately affect women’s ability to progress.

Respecting professional boundaries is therefore essential to building a more equitable environment. Clear boundaries help sustain long-term performance and allow talent to remain and progress within the workforce.

At the same time, the discussion also highlighted the importance of agency. Several speakers noted that actively putting oneself forward, be that asking for opportunities or seeking added responsibility, often opened the door to the most meaningful professional development.

The theme of our discussion was clear. Progress is evident, but the pace of change reminds us that there is still more to do. Businesses have a critical role to play in accelerating that momentum by championing sponsorship, modelling inclusive leadership behaviours and creating environments where talented individuals can thrive at every stage of their careers.

The software sector has found itself back under the spotlight as discussion around GenAI disruption gathers pace. The debate has intensified in recent weeks, after the launch of new AI‑driven tools prompted fresh questions about how quickly established workflows, currently inhabited by software companies, could shift. The accelerating pace at which foundational models are emerging has fuelled a sell-off in public software assets and scrutiny of private markets’ exposure to SaaS models, in both equity and credit.

At Hayfin, this is not a new theme. Early in 2024, we undertook an external review of GenAI‑related risk within our portfolio. Since then, we have embedded the relevant insights into day‑to‑day portfolio management and how we underwrite and invest in new opportunities. While the 2024 review didn’t point to a need for significant change across our portfolio, the result is that our exposure to the space today is deliberate, regularly measured and grounded in a clear view of where software remains resilient.

Across our Direct Lending strategy, software makes up less than 8% of fair value. It is worth recognising that, until very recently, software businesses were among the strongest performers in many institutional portfolios, and for a large number of these companies, the core fundamentals have not changed – they remain well‑run, cash‑generative assets with attractive return profiles. Performance across the software businesses within our portfolio remains in line with expectations. More importantly, this reflects the focus of our exposure: mission‑critical, workflow‑embedded software rather than content generation tools or basic analytics tools or platforms.

These companies sit deeper in customer processes, often underpinning core operational activities where reliability, specificity and domain knowledge matter. In our view, this type of functionality is structurally more difficult to disrupt, even as AI capabilities continue to evolve. Where these businesses also benefit from specialist sponsor ownership, the resilience is further reinforced through disciplined product development and operational support.

A commonly used lens for assessing software business quality is the Rule of 40. It’s a rule of thumb that measures whether a business’s annual revenue growth rate and its EBITDA margin, expressed as percentages and added together, exceed 40. It provides a simple measure of whether a company can balance growth with profitability – two characteristics that, when combined, tend to signal durable market positioning and a more sustainable long‑term operating profile. Businesses that consistently sit above this threshold often demonstrate strong customer value, efficient cost structures and an ability to invest through different cycles.

All companies within our software portfolio currently sit above the 40% benchmark. This is intentional. We prioritise businesses with diversified value propositions, meaningful customer embeddedness and the ability to sustain high margins alongside ongoing growth. We believe these attributes matter more, not less, in an environment where new technologies can alter competitive dynamics.

While industry commentary around GenAI continues to evolve, our approach remains rooted in fundamentals. Our focus is on software that sits at the heart of customer operations, with business models displaying clear relevance and the operational resilience required to manage both periods of change and across cycles. In practice, that means staying disciplined and backing businesses built to endure and generate stable cashflows rather than those chasing short-term momentum or reward.

Our industry is undergoing rapid change. When Tim and I first started Hayfin in 2009, private markets were still in their infancy. The term ‘private credit’ was yet to enter the mainstream. Fast-forward to 2026 and the asset class has grown considerably.

Media, regulators and governments now take a keen interest in what we do. Capital allocations – first from institutional clients, but increasingly from high-net-worths – have risen exponentially. Global private credit AUM has more than trebled in the past decade to over $1.5trn.

In this more mature market, investors are rightly asking their managers what sets them apart from the competition.

We’ve always answered this question with reference to three key competitive advantages:

- Scale

- Adaptability

- Culture

We see these three attributes becoming cornerstones of the industry’s most successful players.

As our platform has evolved over the past year, following the completion of our management buyout and the addition of Mubadala, Samsung Life and AXA IM Prime as shareholders alongside Arctos, these three differentiators ring even truer for Hayfin today.

Why scale matters

Market access has historically been a barrier to entry in private credit. We’ve previously outlined why that’s particularly the case for the fragmented European market.

However, we believe the size of our platform, reach of our network and depth of our proprietary data – gathered over more than 15 years, in the course of investing over €55bn into 500+ companies – should help us to continue retaining and growing lending relationships with high‑performing businesses in the years ahead.

With higher interest rates dragging on transaction activity in the post‑Covid period and slowing deployment for many funds, incumbency has proved a competitive advantage. Approximately half the capital deployed in our direct lending strategy over the past two years has been extended to existing borrowers. With €30bn of assets in the ground today, the opportunity to extend capital to existing borrowers will remain an important source of deal flow for Hayfin. That means we can maintain steady growth independent of broader M&A market cycles.

As AI adoption within private credit accelerates, and technology is increasingly used to crunch numbers and supplement human judgement during the underwriting process, we believe it’s the managers with the largest pools of historic investment data who will be best placed to generate insights.

Finally, we expect the benefits of increased fund sizes and lending capacity to intensify over time. A larger capital base and the ability to make bigger commitments should strengthen GPs’ hands, helping them achieve greater portfolio diversification and negotiate improved terms. With deal sizes continuing to rise, access to capital and close partnerships with blue‑chip LPs will be essential to remaining relevant.

How to adapt amid volatility

With continued volatility across markets and geopolitics, being dynamic and adaptable is crucial. European capital markets are smaller and less efficient than their US counterparts, and the risk‑return trade‑off can shift quickly. To counter this, we have deliberately designed our business to be able to pivot to capitalise on value and opportunity. This is reflected in our broad product suite, which enables us to serve the needs of both borrowers and LPs.

The emerging opportunity within asset‑backed lending is one such example. We are seeing increasing client interest in Europe in asset‑backed deals, as investors become more familiar with private credit and seek more complex, higher‑return and less commoditised opportunities. These types of investments have been a key focus of Hayfin from day one, with €12bn deployed to date, largely through the dedicated expertise we’ve built in sectors such as healthcare, real estate and maritime.

The benefits of flexibility are likely to keep rising alongside the evolution of the asset class. New deployment opportunities should emerge as private credit finances an ever‑increasing cross‑section of European economic activity. That steady expansion of private markets has driven the Bank of England’s inaugural exploratory analysis into how they intersect with the UK real economy, which we’re pleased to be participating in this year.

What a one‑firm culture means

The final ingredient to Hayfin’s success is our single‑firm culture. It has always been our aspiration to be Europe’s most integrated platform. If investors are looking for a multi‑boutique or a ‘pod shop’, there are many fine examples in the market. We aren’t one of them.

The Hayfin team now owns a substantial majority of the GP, and most of our employees are shareholders. This breadth of ownership is an important differentiator for a company of our type and size. That level of independence, autonomy and ownership creates value for LPs by enabling us to continue executing at pace and investing in the next generation of Hayfin leaders.

When we founded Hayfin in 2009, our ambition was to be a first mover capitalising on the emerging opportunity in European private credit. By building scale, resilience and adaptability in a firm that understands the power of collaboration, we believe we have created a platform for all investment environments. In today’s world – characterised by heightened risks and uncertainties alongside abundant opportunity – this flexibility is paramount.

Hayfin continues to be well positioned to support its clients, and I’m excited for what’s to come in the rest of 2026 and beyond.